Core Dash is an insurance broker that can help you enter and buy the price Business insurance Through its partners. After that, you can use a core dash to pay your premium, file claims and update your coverage as needed.

If you have a relatively simple easy insurance requirements – for example, if you need general responsibility or workers’ camp insurance to comply with contracts or state laws – the core dash offers an effective purchase experience. Prices come from leading insurance companies, and the platform provides enough detail to help you make a track.

Unfortunately, you have to buy somewhere else Trade auto insurance. And if you need a very special kind of coverage, such as key person insurance, personal insurance broker is probably your best bet.

Core Dash Insurance: Profession and Conflict

Get numerous prices with a request for general responsibility, professional responsibility, business owners ‘policies, D&O and workers’ camp insurance.

Pay the premium and file claims through the Core Dash platform.

Core Dash Insurance Partners include the top rated business insurance companies of Nairrd Walt, including Chab, Passenger and nationwide nationwide.

No commercial auto insurance.

Core Dash is a brokerage, not insurance company. Your coverage will be provided by a third party.

How Core Dash works

Based on the information you provide, the cost of core dash insurance from several companies. You will need to present:

Basic information such as your name, phone number, email address and business website, if you have.

Your business type, legal structure, industry, address and year were established.

Annual estimated revenue and payroll.

Subsequently, the Core Dash will enter the price from its partners.

Core Dash Insurance Partners

What do you like to get a quote from Core Dash

👋 I am Rosali Murphy, the author of Nairid Walt who covers business insurance. You can be expected when you get a quote from the core dash.

I told the Core Dash that I operated a new, a personal home business as a fluorest and needed general responsibility insurance. I predicted $ 10,000 in annual revenue. (It’s fake; sadly, I’m not flowers from it.)

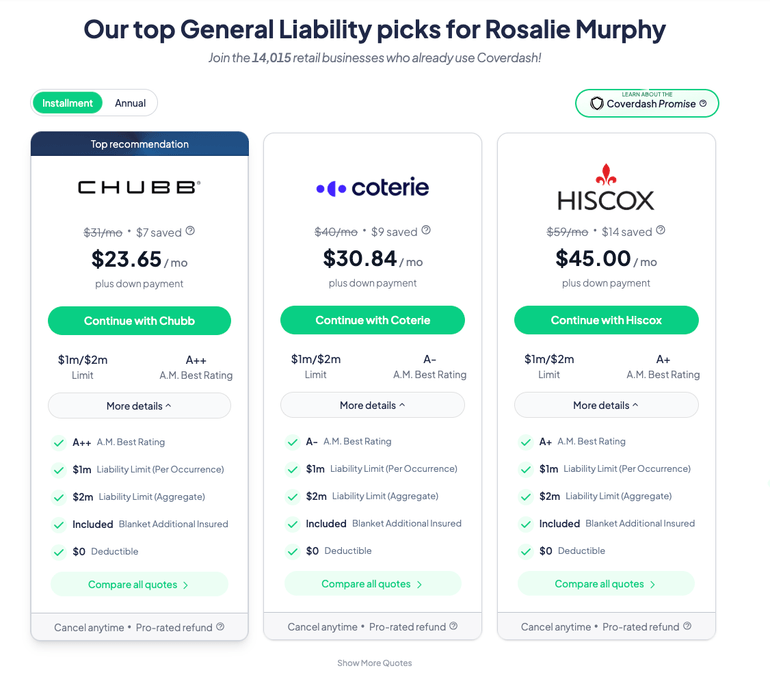

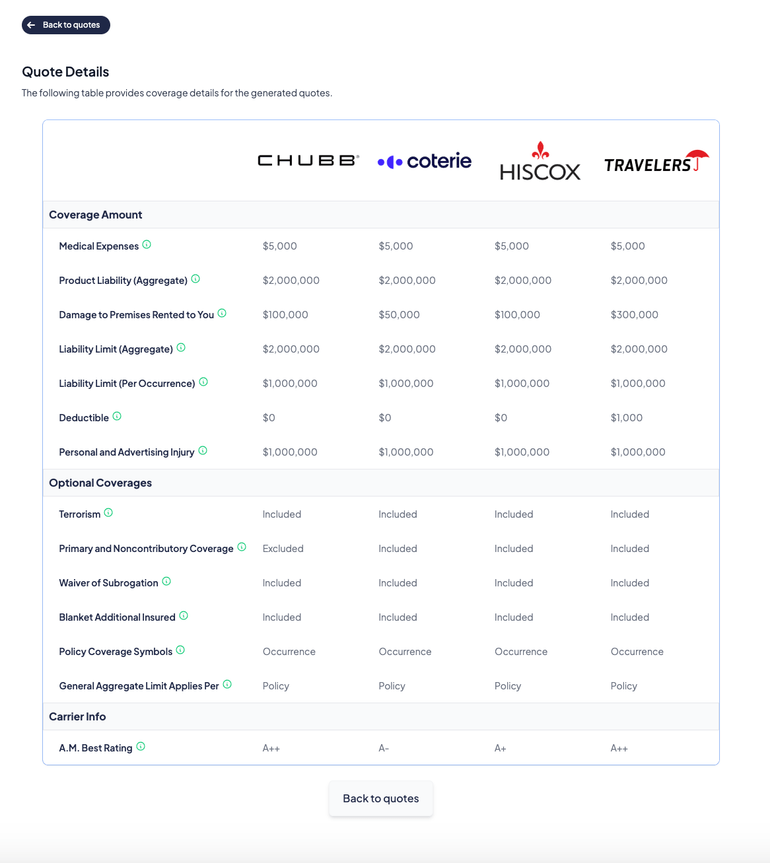

In less than a minute, the service provided multiple prices for a general responsibility policy:

When I dig deep, the Core Dash provided a helper table that allows me to compare coverage limits, deductions and additional defects. This made it easier to identify differences in their price policies:

Overall, these policies are exactly the same. But, for example, the cheapest quote – actually offers more coverage for loss in the rental premises than Kotri, which is slightly more expensive.

However, Chob does not include primary and non -controversial coverage. This means that Chob’s policy will not be played in front of anyone else who may cover the same claim. It doesn’t matter if my fictitious flowers business. However, sometimes coverage is needed for other professions, such as contractors.

Although I did not choose the insurance company, I had to provide contact information to see their references. The next day, by email and with two phone calls, the core dash followed. (Calls did not continue after that, which is always a cause for concern with such services.)

The next day, when I was logged in, my reference was also saved.

Core Dash Insurance: Coverage Types

Through your partners, the core dash offers the following policies:

All Businesses needed: General Responsibility Insurance

In the case of third -party claims of physical injury and property damage, general responsibility insurance protects your business. Nair Walt recommends that all business owners take a policy of general responsibility. You need to get this coverage for some lease and contracts.

🤓 🤓Nerve tip

If your business is a physical place, consider the business owner’s policy instead. The BOPS also includes general responsibility insurance with commercial property insurance, which pays if your luggage is destroyed in a fire -like incident. Most also involve business intervention insurance, which helps you meet your costs when you are repairing and can’t usually work.

For less than $ 10 million in income businesses, Core Dash says there are usually premiums in those limits.

Retail business: $ 700- $ 1,500 annually.

Professional, Scientific and Technical Services: $ 700- $ 1,300 annually.

Wholesale trade: $ 700- $ 2,500 annually.

Residence and food services: $ 1,000-, 000 3,000 annually.

Construction Business: Up to $ 5,000 annually.

Many businesses needed: Workers’ compensation

In most states the need for workers neededAlthough which companies need it, it varies by industry and how many employees do you have. Coverage is kicked if one of your employees is injured and needs medical care and time to recover.

Expenditures by the workers Your industry can vary widely. For example, construction business costs the most because construction workers are usually at higher risk of injury than retail workers.

For less than $ 10 million in income businesses, Core Dash says workers’ compositions that sell it usually have premiums within those limits.

Retailer $ 500- $ 1,600 annually.

Wholesale trade: $ 500- $ 1,600 annually.

Residence and food service: $ 900- $ 2,500 annually.

Construction: $ 1,000- $ 10,000 annually (varies by state and what services the company provides)

Many businesses needed: professional liability insurance

Professional Liaison Insurance, which is also known Mistakes and errors insuranceIf a client accuses you of negligence or inadequate work, protects your business. If you provide users for fees, you should have E&O insurance.

For less than $ 10 million in revenue businesses, Core Dash says that professional responsibility policies are usually premiums in those limits.

Professional, Scientific and Technical Services: $ 800- $ 3,500 annually.

Construction (a specific E&O policy for contractors): 200 1,200- $ 5,000 annually.

Technology: 3 1,300- $ 2,400 annually.